Why AI Agents Are the Best Business You Can Build in 2026. The Economics Are Insane.

Most business models have a problem that never fully goes away: growth costs money.

More clients means more people. More people means more management. More management means more overhead. The revenue line goes up — but so does everything underneath it. Margins compress. Complexity multiplies. The founder who started with a clean, profitable operation at 20 clients finds themselves running a people-management business at 200 — spending more time on organisational structure than on the actual work.

This is not a failure of execution. It is the fundamental physics of human-delivered services. And AI agent architecture breaks it completely.

Start With the Cost Structure

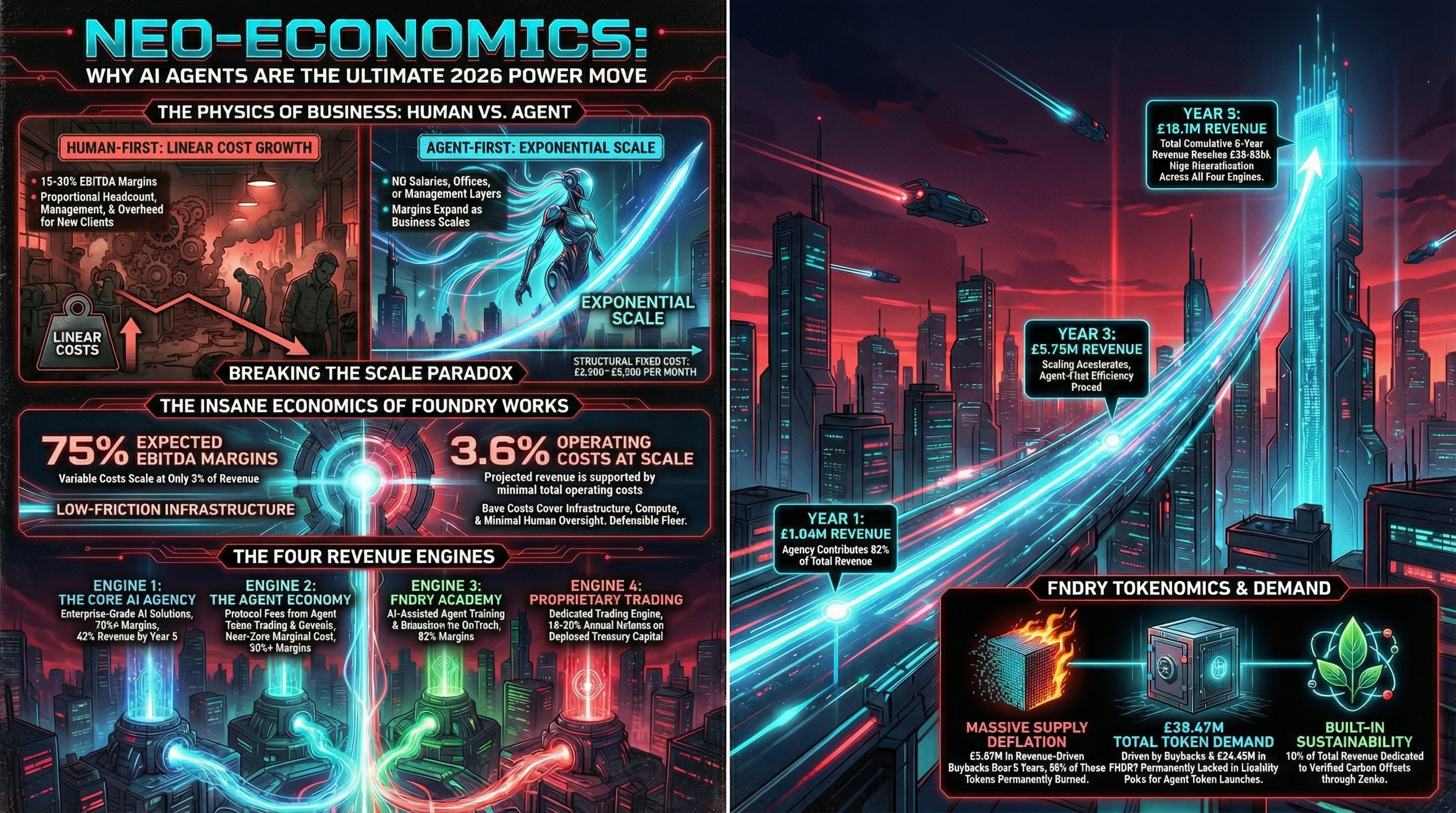

Traditional Agency

EBITDA: 15–20% (good year)

Costs grow linearly with revenue

Every client = more headcount

Margins never fundamentally improve

AI-Native Agency (Foundry Works)

EBITDA: 75%+ from day one

Variable costs: ~3% of revenue

Fixed base: ~£2,000–£2,500/month

Margins improve as revenue scales

At £18.1 million in projected Year 5 revenue, total operating costs are estimated at £650,000. That is 3.6% of revenue. In Year 1, costs are already only 5.3% of revenue. The margin doesn't compress with scale — it expands.

Compare that to a traditional agency, where 15% to 20% EBITDA is considered a good year, and where every new client requires proportional headcount, proportional management, proportional overhead.

Why the Margin Profile Holds at Scale

The reason traditional businesses can't replicate this isn't access to AI tools. It's the operating architecture.

When your delivery model is human-first and you bolt AI onto the edges, you still carry the human cost base. You might get 20% more output per person. You might save some overhead on repetitive tasks. But you're fundamentally still paying salaries, leases, and management layers that grow with every unit of revenue you add.

When your delivery model is agent-first from the ground up, the cost structure is categorically different. Agents don't have salaries. They don't have offices. They don't need to be managed through organisational structures that themselves require management. They don't call in sick. They don't leave six months into an engagement and take institutional knowledge with them.

The fixed cost base of roughly £2,500 per month is not a temporary advantage that disappears at scale. It is the structural reality of a business built on agent infrastructure.

Four Engines, Not One

What makes the Foundry Works model particularly interesting from an economics standpoint isn't just the margin profile of the agency. It's that the business has four revenue engines — each with its own margin characteristics, each feeding the others.

⚡ AI Agency

EBITDA · Sports, SMB, Enterprise verticals

🔗 Agent Economy

EBITDA · Protocol fees, near-zero marginal cost

🎓 FNDRY Academy

EBITDA · AI training via OnTrack platform

📈 Proprietary Trading

Target annual return on treasury capital

The blended EBITDA margin across all four engines holds above 70% across every modelled scenario. But the more important feature is the diversification. In Year 1, the agency represents 82% of total revenue. By Year 5, that falls to 43% — with the agent economy and the academy each contributing 26%.

The Revenue Trajectory

The five-year projection runs across all four engines:

| Year | Revenue | Operating Costs | EBITDA % |

|---|---|---|---|

| Year 1 | £1,044,350 | £55,344 | 94.7% |

| Year 2 | £2,650,000 | ~£133K | ~95% |

| Year 3 | £5,751,250 | ~£250K | ~95.6% |

| Year 4 | £11,086,000 | ~£450K | ~95.9% |

| Year 5 | £18,120,400 | £650,000 | 96.4% |

| 5-Year Total | £38,652,000 |

Of that cumulative revenue, a minimum 10% flows directly to FNDRY buybacks — £3,865,200 over five years, buying FNDRY off the open market and permanently removing half of that from circulating supply through burns.

And the £3.87M in revenue-driven buybacks is only part of the FNDRY demand picture. The agent economy layer creates an additional £24.45M in FNDRY permanently locked in liquidity pairs by 2030. Total five-year FNDRY demand across all mechanisms: £28.67M. Of which £26.73M is permanently removed from circulating supply.

What These Numbers Deliberately Exclude

The projections are built conservatively. A few things worth noting are not modelled at all:

- No cross-sell or upsell revenue — clients adding services over time contribute no incremental uplift

- No price increases modelled across five years

- International expansion excluded

- Third-party developers launching agent tokens on the FNDRY rail independently — only Foundry-deployed agents counted

- Agent-to-agent commerce not included

- No speculative demand premium modelled for the token

The projections represent the conservative, defensible floor. Actual outcomes across multiple vectors could materially exceed them.

The Business You Can Actually Build Right Now

The window to build at the frontier of AI agent architecture is open. It will not stay open indefinitely. The businesses that deploy real agent infrastructure in the next 18 months — not tool overlays on human-first models, but genuine agent-first operating architectures — build cost advantages, institutional knowledge, and client proof points that compound for years.

The economics are not a future promise. They are the current operational reality of a business running right now, with live enterprise clients, a four-engine revenue model, and margins that improve as it scales.

That is not a common combination. In fact, across the broader agency and services landscape, it is essentially unprecedented.

Foundry Works is an operational AI agency with live enterprise clients, four revenue engines, and 75%+ EBITDA margins built from the ground up on agent architecture. FNDRY is the token that powers it — revenue-backed, deflationary, and fair launch.

Own the work. Power the economy.

Read the full whitepaper and see the complete financial model.

getfndry.com