$7.84 Billion to $52 Billion in 4 Years. What the AI Agent Boom Actually Means for Businesses Right Now.

There's a number that should stop you mid-scroll.

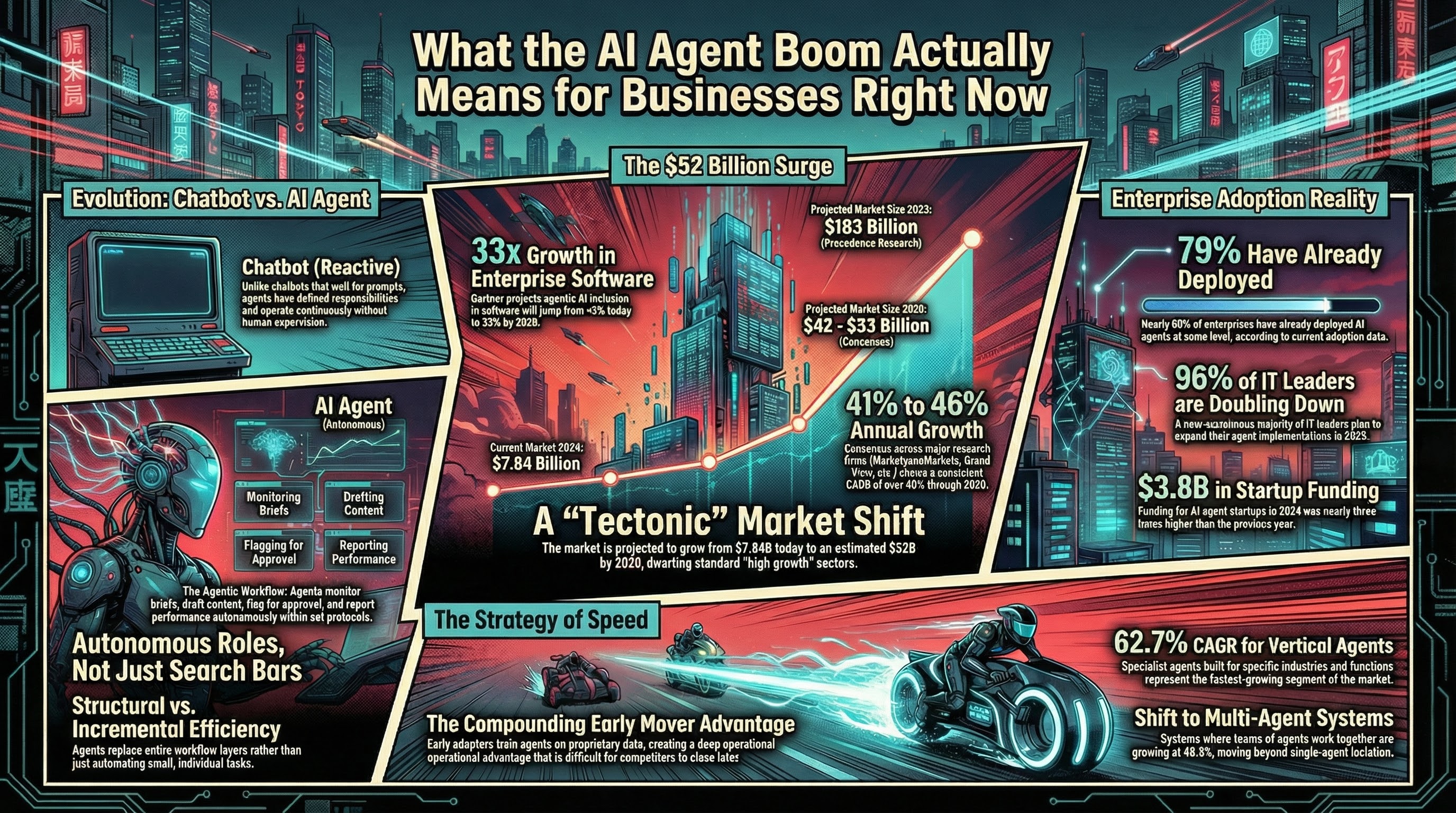

Gartner — not a crypto research firm, not a speculative analyst house, not a VC talking their own book — projects that 33% of all enterprise software will include agentic AI by 2028. Today that number is less than 1%.

A 33-fold increase. In four years. From one of the most conservative forecasting organisations in the technology industry.

That's not a trend. That's a tectonic shift. And most businesses are standing directly in its path without realising it.

The Numbers, Laid Out Plainly

The AI agent market sits at approximately $7.84 billion today. By 2030, the consensus across MarketsandMarkets, Grand View Research, BCC Research, and MarkNtel Advisors puts it somewhere between $42 billion and $53 billion. The compound annual growth rate across those forecasts holds consistently at 41% to 46%.

For context: most "high growth" markets that get breathlessly covered in the financial press are growing at 15% to 20% annually. The AI agent market is growing at more than double that. Every year.

And Precedence Research — taking the longer view to 2033 — puts the number at $183 billion, at a 49.6% CAGR. Aggressive? Maybe. But so was anyone who projected smartphone adoption in 2008.

The enterprise adoption data makes the market sizing feel conservative rather than optimistic. 88% of enterprises already report regular AI use. 79% have deployed agents at some level. 96% of IT leaders plan to expand their agent implementations in 2025. AI agent startups raised $3.8 billion in funding in 2024 alone — nearly three times the prior year.

This isn't a technology that enterprises are evaluating. It's one they're already running. The question isn't whether adoption happens. It's how fast, how deep, and who captures the value.

What "AI Agent" Actually Means in Plain English

The term gets thrown around loosely enough that it's worth being precise about what we're actually talking about — because the distinction matters for understanding why the growth numbers are what they are.

An AI agent is not a chatbot. It's not a smarter search bar. It's not a tool that waits for a human to prompt it and then generates a response.

An AI agent has a role. It has defined responsibilities. It operates continuously, autonomously, and within a framework of rules and escalation protocols — taking actions, making decisions, and completing work without a human needing to supervise every step. A content agent doesn't wait to be briefed. It monitors briefs, drafts content, flags for approval, schedules distribution, and reports on performance. A sales agent doesn't wait for a lead list. It researches prospects, personalises outreach, manages follow-up sequences, and hands off to a human only when the conversation requires it.

The reason enterprise adoption is accelerating at the rate Gartner describes is because businesses are discovering that agents don't just automate tasks — they replace entire workflow layers. The efficiency is not incremental. It is structural.

McKinsey's 2025 State of AI report found that 23% of organisations are actively scaling agentic AI, with another 39% in active experimentation. No function has more than 10% of respondents at full scale yet — which means the adoption curve has enormous runway remaining even among companies already engaged.

Why This Matters Now, Not in Three Years

There's a failure mode in how most businesses process data like this. They read the projections, nod at the opportunity, add it to a "things to explore" list, and return to the immediate operational pressures of the week. Three years later, a competitor has structurally rebuilt their cost base around agent architecture and the gap has become very difficult to close.

The early mover advantage in AI agent adoption is real and it compounds. The businesses deploying agents now are training them on proprietary data, building institutional knowledge into their AI infrastructure, and developing the internal expertise to iterate and improve. That three-year head start does not evaporate when everyone else finally gets serious.

The vertical AI agent segment — specialist agents built for specific industries and functions — is the fastest growing within the broader market, at 62.7% CAGR. Multi-agent systems, where teams of agents work together rather than a single agent operating in isolation, are growing at 48.5%. These aren't the easy, generic applications. They're the ones that create the deepest operational integration and therefore the most durable competitive advantage.

The Foundry Works Position

Foundry Works launched into this market with a specific thesis: businesses don't need another AI tool to add to their stack. They need an AI team — agents with defined roles, working together, integrated into their actual operations.

Lenovo ISG and Brother International signed as enterprise clients in the first two weeks of operation. Not because the pitch was clever. Because the economics are so structurally compelling that a rational business decision-maker cannot look at the alternative and justify it.

The AI agent market growing from $7.84 billion to $52 billion isn't a macro story happening somewhere else. It's the specific market that Foundry Works operates in, is positioned to serve, and is building infrastructure to power — through the agency, through the agent economy, through FNDRY.

The growth validates the model. The model captures the growth. That's the flywheel.

Foundry Works is an operational AI agency with live enterprise clients, four revenue engines, and 75%+ EBITDA margins built from the ground up on agent architecture. FNDRY is the token that powers it — revenue-backed, deflationary, and fair launch.

Own the work. Power the economy.

Read the full FNDRY whitepaper and see what an AI agency actually looks like in production.

foundryworks.ai